As the global economy continues to fluctuate in reaction to the COVID-19 pandemic, PERA members continue to inject over $4 billion into the state and local economies. The economic role PERA retirees play in the areas in which they live is the focus of the recently released Economic and Fiscal Impacts 2020 report, prepared by Boulder-based Pacey Economics, Inc.

The Value of a Defined Benefit Plan

In a Defined Benefit plan, employee and employer contributions go into a trust. Funds in this trust are invested. Any investment returns increase the trust’s overall value. Funds in the trust are used to pay retiree benefits.

Economists at Pacey calculated that PERA employer contributions account for about three percent of the overall budgets of participating employers. Once those contributions arrive at PERA, they get put to work. Over the past three decades, investment returns have been the largest source of additions to the fund (61%), ahead of employer contributions (22%) and employee contributions (17%).

“We feel that this is a much more efficient use of money than a 401k plan or Social Security,” said Jeffrey E. Nehls, an economist at Pacey Economics. “If we were to put the same money in a 401k or Social Security, we wouldn’t have as good of an outcome, as much money for retirees to spend.”

Nehls said that Social Security is a regressive benefit. Middle-class income earners in Social Security recoup a smaller percentage of their total contributions compared to PERA retirees. One contributing factor is the way in which contributions are invested. “Social Security is required to invest in Treasuries,” he said. “So, they don’t earn as much interest on their earnings compared to PERA, making it a much less efficient use of contributions.”

Taking the Guesswork Out of Retirement

Nehls added that a retiree with a Defined Benefit plan doesn’t need to guess about longevity when making a retirement budget, while a person relying on a defined contribution plan like a 401(k) does. Those in a defined contribution plan must predict how long they might live when determining how much to withdraw each year. Erring on either side has financial consequences. Overestimate your lifespan, and you curtail your spending and leave money on the table. Underestimate, and you find yourself without needed income later in life.

It’s unlikely any person can guess their lifespan in advance, so most people will end up overestimating or underestimating to a certain degree. “But in a Defined Benefit plan,” Nehls said, “you avoid that problem of having to adjust risk in spending.”

Additionally, 401(k) plans are less efficient because participants often dial down risk, and potential returns, as they near retirement, as well as throughout retirement. Funds in a Defined Benefit plan can remain more fully invested in investments with higher potential returns.

The PERA Retiree Impact on Colorado’s Economy

The report illustrates the ways in which retirees are an integral part of their local economy. Because 106,059 PERA retirees live in Colorado, the statewide effect is significant.

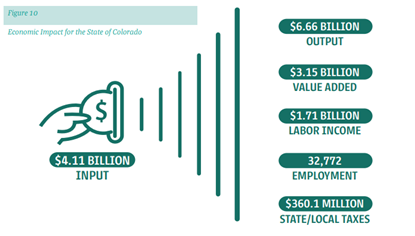

Nehls said that if he had to convey this concept with a single image from the report, he would choose this one:

This image details how the income PERA retirees receive ($4.11 billion in 2019) ends up producing $6.66 billion in economic output. That’s because retiree income has, in the language of economics, a high velocity of money.

Velocity of money is a measure of how many times a dollar gets moved from person to person during a set amount of time.

Someone who is employed might save some for retirement, save some for a down payment on a home or car, save some for a college fund for a child. Saving money is good for the individual in this instance, but it removes money from actively flowing through the economy. This results in a low velocity of money.

On the other hand, retirees, especially those who receive a steady income, tend to spend a higher percentage of their income as long-term saving is less of a priority. This results in a high velocity of money, which can have powerful downstream effects. Pacey economists calculated that retiree spending in Colorado results in supporting 32,772 jobs.

A Constant Amid Uncertainty

“The other big takeaway,” Nehls added, “is that when there is an economic downturn, like the one we are experiencing now, retiree spending acts as a huge stabilizer. People in a Defined Benefit plan like PERA have the same paycheck every month. While some people lose some or all of their income, retirees have money to keep the economy going. A Defined Benefit plan is not volatile, unlike the labor market or stock market.”

This stabilizing effect is especially important in Colorado’s rural areas, where retiree income makes up a greater share of area payroll. In 26 Colorado counties (nearly all rural), these distributions represent at least 10 percent of the county’s total payroll.

PERA retirees play an integral role in their communities. They provide leadership. They continue to do important work, often volunteering their time. The economic benefit they provide is another way in which their communities rely on them. As the introduction to the report states, “the stability and size of PERA’s monthly benefit payments will continue to grow and help Colorado’s economy weather and recover more quickly than if this 89-year investment by Colorado wasn’t continued and secured on behalf of the citizens of the state and for our civil servants who help us all to continue to make our wonderful home of Colorado better.”

Highlights of the Economic and Fiscal Impact Study of Colorado PERA—State of Colorado

Defined benefitAlso known as a pension, this is a type of pooled retirement plan in which the plan promises to pay a lifetime benefit to the employee at retirement. The plan manages investments on behalf of members, and the retirement benefit is based on factors such as age at retirement, years of employment and salary history.Defined benefitAlso known as a pension, this is a type of pooled retirement plan in which the plan promises to pay a lifetime benefit to the employee at retirement. The plan manages investments on behalf of members, and the retirement benefit is based on factors such as age at retirement, years of employment and salary history.Defined contributionA type of individual retirement plan in which an employee saves a portion of each paycheck (along with a potential employer match) and invests that money. The employee’s retirement benefit is based on their account balance at retirement. A 401(k) is a type of defined contribution plan.

PERA has made it impossible to receive SS disability even though I qualify and paid SSI for 25 years!

I’m not a fan. It has cost me thousands of $$ I needed for medical.

PERA retiree not only provide a huge amount t of the ecomomy in Colorado but every wahereelsse they live. I

I Ilive outside of Colorado and I pay .a big amount on taxes on money I earned in Colorado not here where I live. .

It is certainly true that pension monies are spent with local economies to great benefit. It’s also true that this impact is affected negatively when pensions are reduced by the elimination or drastic reduction of annual increases. So it would be easy to calculate the estimated loss to local economies of potential benefit lost by pensions falling behind cost of living. When a 3.5% annual increase is reduced to zero, the positive contribution to the local economies is reduced by 3.5%….. probably more.